The Multichain World and the Stablecoins

The multichain world arrived in 2021.

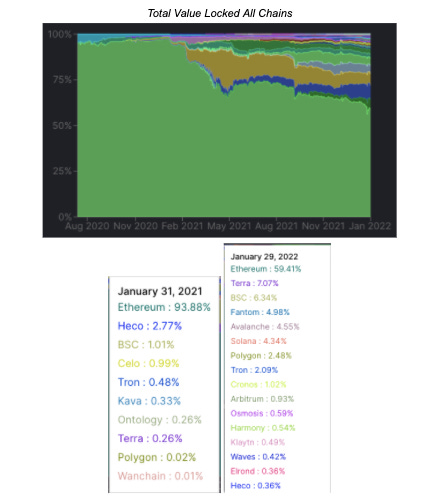

One year before, Ethereum had a supremacy, representing around 94% of the Total Value Locked (TVL) in all chains.

Source: https://defillama.com/chains

In practice, Ethereum was the only land to build your project.

A good analogy is, each chain, one neighborhood in the blockchain city.

Ethereum is one rich neighborhood, where we can find many millionaires and sophisticated stores. There is much wealth in that area. As it happens in rich neighborhoods it is very expensive to build there and open your business.

In 2021, we also saw in the neighborhood of Ethereum new buildings increasing the supply of space there. These are the Layer-2s like Arbitrum and Optimism. They already have almost $2 billion in TVL. For example, Rari Capital launched Fuse Pools on Arbitrum this month.

You can see by the figure below, the cost to transfer ETH using Aribitrum and Optimism is 20% of using Ethereum. In our analogy, it would be the difference of living in an apartment on that neighborhood or in a house.

Source: https://l2fees.info/

In 2021, we also saw a relevant TVL increase from new neighborhoods, such as Avalanche and Fantom. This had a big impact on the market share of Ethereum that fell from 94% to 59%. In the new chains, the cost to make a transaction is less than $1.

It is interesting to note in the figure below that not only the TVL in other chains increased a lot, but also the number of projects in each chain. I highlight Avalanche, Fantom and Polygon that have more than 100 projects there.

Source: https://defillama.com/chains

Another metric to observe is the dominance from the lead project in each chain. In the case of Avalanche, Aave represents 27% of TVL, in Fantom, Multichain represents 58% and in Polygon Aave dominance is 45%. It is better to have a more diversified TVL than to be concentrated in just one project.

There are two different approaches in creating a new neighborhood. Building in a completely isolated place and far from the rich land of Ethereum or building very close to Ethereum neighborhood and facilitating the connection with it. Solana took the first approach and because of that the projects we see there are not in other chains. Avalanche and Fantom chose the latter approach, creating an EVM compatible chain that makes it easier for developers to open new branches of their projects in these new neighborhoods. That's why we can see in those chains many projects that come from Ethereum.

DeFi projects are expanding as a supermarket opening new stores in other neighborhoods.

The new neighborhoods need stablecoins, the base of DeFi. On its turn, the stablecoins need the neighborhoods to grow, a land with lesser costs.

To be more inclusive and open for everyone, DeFi needs to reduce the transaction costs.

So the first thing to a multichain stablecoin is to be available in the new promising neighborhoods as soon as possible. The USDC, for example, adopted the multichain strategy and is available in many chains. Ethereum is the main one with 44 billions USDC. In December, USDC launched on Avalanche and it already has 67 million there.

The native stablecoins tend to be more secure to users than bridged assets from other chains. For decentralized stablecoins, the challenge is to offer native stablecoins in each chain, while keeping the peg. It needs a good system to transfer the reserves value between chains.

Another interesting move from stablecoins is to make partnerships with the main projects of each chain. For example, if a project wants to expand to the Harmony neighborhood it would be interesting to make partnership with DeFi Kingdom, a leading project there. Another example would be if the Tribe deploys Rari Capital Fuse Pools and FEI in other chains, helping DAOs in other chains to thrive.

I am very curious to see what will happen this year. Come with me and I will tell you what I am seeing in the development of this blockchain city, full of opportunity and risks.

Thank you for your attention.

P.S.: Thanks for the comments from DioDionysos.

Please note that this letter is not intended as financial advice.